Nvidia stock produced life-changing returns over the past two decades, but Wall Street analysts still see upside for shareholders.

Nvidia (NVDA 3.71%) accomplished a great deal in the past two decades. The chipmaker solidified its status as the gold standard in graphics processors for video games and other multimedia. Moreover, its accelerated computing platform has become the premier solution for demanding data center workloads like analytics, artificial intelligence, and scientific simulation.

During that period, Nvidia saw its share price soar 45,900% as it transitioned from computer graphics trailblazer to data center powerhouse. To contextualize that figure, $10,000 invested in Nvidia in April 2004 would now be worth about $4.6 million.

The stock has been especially hot lately, with shares tripling in the past year alone. Even so, Wall Street is still overwhelmingly bullish on Nvidia. The stock carries a consensus rating of “buy” and its median one-year price target of $1,000 per share implies 22% upside from its current price. Even more compelling, among the 60 analysts that follow Nvidia, not a single one recommends selling right now.

Here’s what investors should know.

Nvidia dominates the market for accelerated computing solutions

Nvidia is best known for inventing the graphics processing unit (GPU), a chip now synonymous with ultra-realistic 3D graphics and accelerated computing, a discipline that uses specialized hardware to speed-up demanding data center workloads like artificial intelligence (AI) and data analytics. To quantify its success, Nvidia holds more than 95% market in workstation GPUs, 94% market share in data center GPUs, and more than 80% market share in AI processors, according to analysts.

However, Nvidia is more than a GPU company. Its data center hardware portfolio also includes the Grace central processing unit (CPU) and high-performance networking platforms purpose-built for AI. Additionally, Nvidia has broadened its ability to monetize 3D graphics and AI by delving into subscription software and cloud services.

Nvidia AI Enterprise is a suite of development tools, software frameworks, and pretrained models that help businesses build all manner of AI applications, including computer vision, conversational intelligence, and recommender systems. Additionally, DGX Cloud pairs Nvidia AI Enterprise software with supercomputing infrastructure to create a comprehensive AI-as-a-service offering.

Similarly, Nvidia Omniverse Cloud comprises hardware, software, and services for 3D application development. It also serves as a simulation engine capable of training and evaluating machine learning models for autonomous robots and self-driving cars. Additionally, Omniverse includes tools for developing interactive avatars that address use cases like non-playable video game characters and digital customer service agents.

In short, Nvidia’s robust accelerated computing platform comprises hardware, software, and services that position the company as a one-stop shop for 3D graphics and artificial intelligence. CFRA analyst Angelo Zino says that full-stack strategy affords Nvidia an “incredible competitive moat.”

Nvidia followed a strong fourth quarter with a wave of product announcements

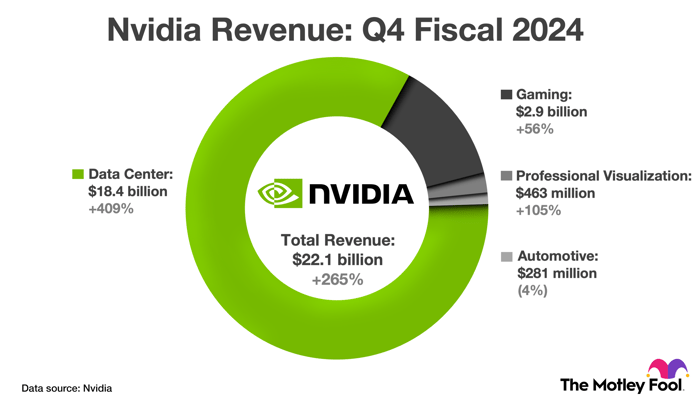

Nvidia reported impressive financial results in the fourth quarter, crushing estimates on the top and bottom lines. Revenue climbed 265% to $22.1 billion, gross profit margin expanded 10 percentage points, and non-GAAP net income soared 486% to $5.16 per diluted share.

The impetus behind that stellar performance was strength in the data center category, something CEO Jensen Huang attributed to two tailwinds. First, data centers are transitioning from general purpose to accelerated computing. Second, data centers are investing aggressively in the computing infrastructure required to support generative AI.

The chart below provides more detail on Nvidia’s fourth-quarter revenue across its four primary product categories.

The chart shows revenue growth across Nvidia’s four largest product categories in the fourth quarter of fiscal 2024 (ended Jan. 28, 2024). OEM & Other revenue has been excluded because it accounted for less than 1% of total revenue.

Nvidia announced several noteworthy products at its annual GPU Technology Conference (GTC) in March. The headline announcement was its latest GPU architecture, Blackwell. “Generative AI is the defining technology of our time. Blackwell is the engine to power this new industrial revolution,” said CEO Jensen Huang.

Additionally, Nvidia announced a new superchip that pairs Blackwell GPUs and Grace CPUs, new high-performance networking platforms, and its next-generation supercomputer for autonomous vehicles. The company also announced Project Groot, which comprises a machine learning model and supercomputer purpose-built for humanoid robots.

Wall Street expects strong earnings growth, but Nvidia stock is far from cheap

Going forward, the graphics processor market is forecasted to grow at 28% annually through 2030, and AI spending across hardware, software, and services is projected to increase at 37% annually during the same period. That gives Nvidia a good shot at 30%-plus annual sales growth through the end of the decade, which implies similar earnings growth.

Indeed, Wall Street analysts expect the company to grow earnings per share at 35% annually over the next five years. In that context, its current valuation of 69 times earnings sits somewhere between reasonable and expensive. In other words, patient investors can buy a very small position in this stock right now, but it may be more prudent to wait for a slightly cheaper valuation.